Filtronic ($FTC.L) [Investing]

The company specializes in mission-critical communication subsystems for the space, aerospace, defense, and telecommunications infrastructure sectors.

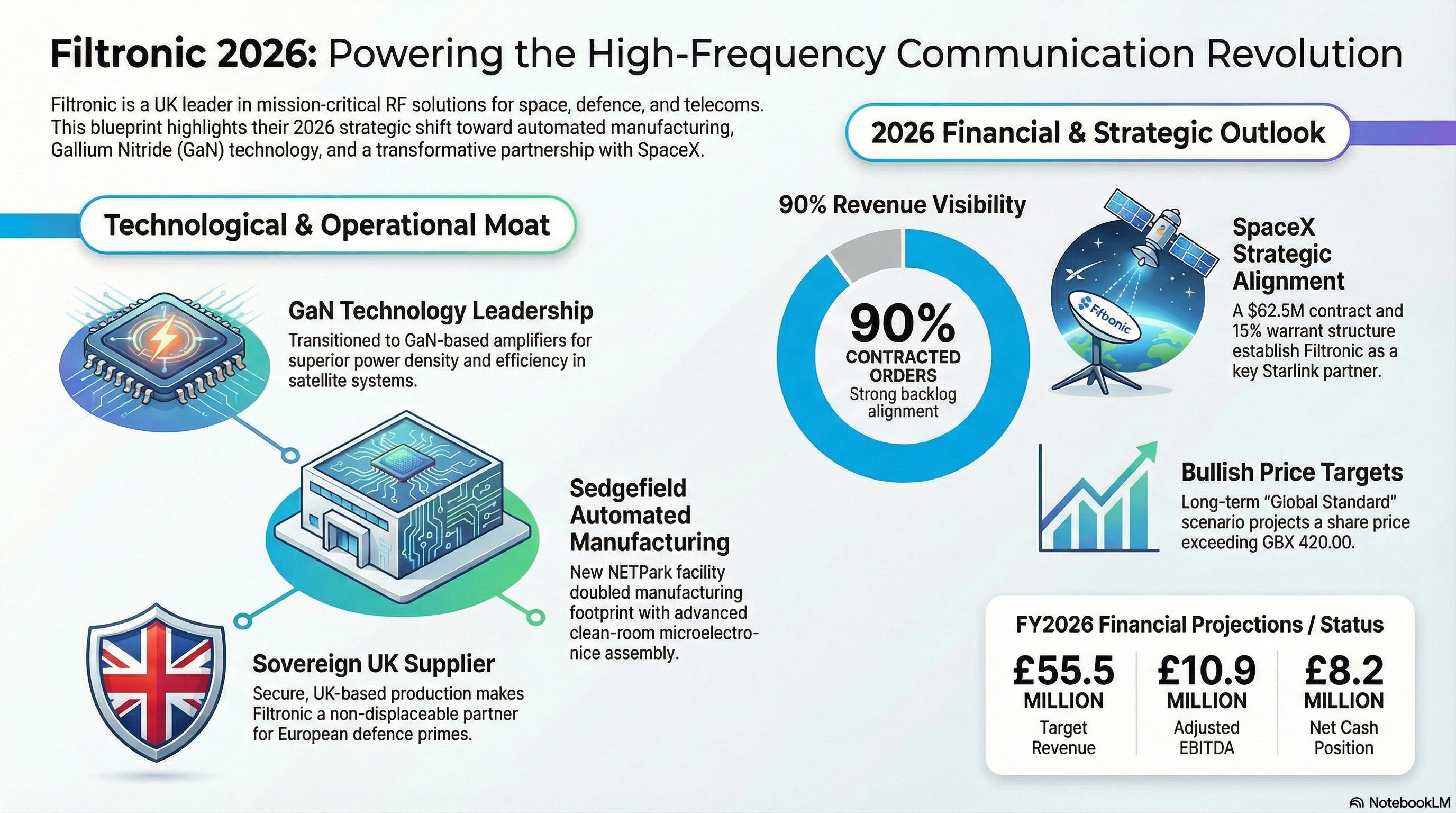

Filtronic is a UK-based designer and manufacturer of advanced radio frequency (RF), microwave, and millimeter-wave (mmWave) solutions. The company specializes in mission-critical communication subsystems for the space, aerospace, defense, and telecommunications infrastructure sectors.

1. Advanced RF & mmWave Hardware

Filtronic’s edge lies in managing complex signals at ultra-high frequencies where traditional electronics fail.

Gallium Nitride (GaN) Technology: In 2025–2026, Filtronic finalized its transition toward GaN-based amplifiers. These offer significantly higher power density and efficiency compared to legacy Gallium Arsenide (GaAs), which is critical for the next generation of satellite and radar systems.

Solid State Power Amplifiers (SSPA): Filtronic has pioneered high-power SSPAs, including a 550W Ka-Band SSPA developed under the UK Space Agency’s National Space Innovation Programme (NSIP). These are designed to replace bulky Traveling Wave Tube Amplifiers (TWTAs) in satellite ground stations, offering better reliability and lower maintenance.

Spectrum Expansion (E, V, & W-band): The company is a leader in E-band (70/80GHz) and is expanding into V-band and W-band. This provides the massive bandwidth required for Low Earth Orbit (LEO) satellite constellations and high-capacity 5G/6G backhaul.

2. Sovereign Manufacturing & Automation

Filtronic differentiates itself through its “Design for Manufacture” philosophy and its specialized UK-based production capabilities.

Sedgefield Facility (NETPark): In early 2026, Filtronic ramped up operations at its new headquarters in Sedgefield, UK. This facility doubled the company’s manufacturing footprint and features advanced clean-room areas and automated microelectronics assembly.

Sovereign Accreditation: As a UK-based firm with secure facilities, Filtronic serves as a “sovereign” supplier for European and UK defense primes, ensuring that critical communication components are produced within secure, friendly borders; a major priority for defense spending in 2026.

3. Strategic Partnerships & Diversification

Filtronic has shifted from a niche component maker to a strategic partner for global aerospace giants.

SpaceX Partnership: A transformative relationship with SpaceX (including a $62.5M record contract for E-band technology) established Filtronic as a key supplier for the Starlink constellation. As of 2026, SpaceX holds a roughly 10% vested interest in Filtronic.

Defense Momentum: In late 2025, the company secured an £11 million contract with a major European defense prime for electronic sensor programs, proving its ability to diversify revenue beyond commercial space.

I. Market & Analyst Sentiment

As of February 2026, market sentiment is highly bullish on technical capability, though analysts are closely watching the company’s margins as it balances heavy reinvestment with rapid scaling.

A. The Bull Case: GBX 215.00 – 225.00 (The “Space Infrastructure” Play)

Bulls argue that Filtronic is the “picks and shovels” provider for the modern space race.

Order Book Visibility: With approximately 90% of FY2026 revenue already covered by contracted orders as of February 2026, bulls see very low execution risk.

Strategic Moat: Analysts note that Filtronic’s GaN E-band technology is difficult to replicate, positioning them as a mandatory partner for any major LEO constellation (Amazon Kuiper, OneWeb, etc.) looking to compete with Starlink.

Operational Scale: The move to the automated Sedgefield facility is expected to drive significant margin expansion by late 2026 as production volumes increase.

B. The Consensus View: GBX 195.00 – 210.00 (Growth vs. Valuation)

The consensus reflects a “Buy” or “Strong Buy” but acknowledges the stock’s rapid appreciation over the last two years.

Investment Cycle: While revenue is surging (projected at ~£55M for FY2026), adjusted EBITDA has seen a temporary dip due to planned investments in “people, facilities, and product development.”

Valuation: With a forward P/E ratio around 48x, some analysts suggest the stock is “fairly valued” until the company proves it can maintain high margins while diversifying its customer base.

C. The Bear Case: GBX 140.00 – 160.00 (Concentration Risk)

Bears focus on the company’s reliance on a few “mega-customers” and the risks of a capital-intensive business model.

SpaceX Dependency: Despite defense wins, SpaceX remains a dominant portion of the order book. Bears fear that any change in Elon Musk’s vertical integration strategy could leave Filtronic with massive overcapacity.

Margin Compression: Bears worry that the competitive nature of the defense sector and the high costs of maintaining a sovereign UK facility could lead to lower-than-expected profitability if volume growth slows.

II. Financial Health & Strategic Resilience (Q1 2026)

Following its transformative 2025 performance and the opening of its high-capacity Sedgefield facility, Filtronic’s financial strategy has pivoted toward sustainable scaling and customer diversification. While the company is navigating a “digestive” period of heavy reinvestment in early 2026, its balance sheet remains robust with no long-term debt and a clear path to multi-sector growth.

1. Cash Runway & Investment Management

Liquidity Position: As of the Q1/H1 2026 reporting period (ending November 30, 2025), Filtronic maintained a healthy cash position of £10.5 million. This is a strategic drawdown from the £14.5 million held in May 2025, primarily due to the self-funded relocation to its new headquarters and manufacturing hub.

Self-Sustained Growth: Unlike many peers in the space-tech sector, Filtronic is not reliant on external capital raises. Net cash (excluding property leases) stood at £8.2 million, providing a solid buffer for R&D into W-band and GaN technology.

Operational Efficiency: Cash generation remains a strength, with £3.4 million generated from operating activities in H1 2026, a significant increase from £2.1 million in the prior year, despite the heavy facility transition costs.

2. Backlog Quality & Revenue Visibility

Record Order Book: Filtronic entered the second half of FY2026 with its largest-ever order book. Crucially, 90% of the full-year 2026 revenue target is already covered by contracted orders, providing exceptional visibility for analysts.

SpaceX Anchor & Beyond: While a $62.5 million SpaceX agreement remains the cornerstone of the backlog, the quality of revenue is improving through diversification. New multi-year deals include a €7.0 million satellite constellation contract and a £13.4 million defense sensor program.

Revenue Phasing: Market consensus for FY2026 (ending May 31) targets revenue of £55.5 million. While this is broadly flat compared to the outlier growth of FY2025 (£56.3M), it represents a more balanced and “sticky” revenue mix as the company transitions from one-off peak deliveries to recurring program roles.

3. Capex to Margin Intensity

Facility Scaling: The move to the new Sedgefield site has doubled the manufacturing footprint. Management anticipates that the automation and increased throughput of this facility will be the primary driver for margin recovery in late 2026 as the initial setup costs are absorbed.

EBITDA Evolution: Adjusted EBITDA for FY2026 is projected at £10.9 million (down from the £17.0M peak in FY2025). This planned contraction reflects a deliberate 29% increase in headcount and engineering investment to support the 2026-2027 product roadmap.

R&D Funding: Financial resilience is further bolstered by non-dilutive government grants, including a recent £1.2 million award from the UK Space Agency for Ka-band SSPA development, allowing the company to innovate without impacting the bottom line.

III. 2026 Catalysts to Monitor

A. Tailwinds

Next-Gen GaN Product Launch: Scheduled for calendar year 2026, the rollout of Filtronic’s proprietary GaN E-band products (including the £47.3M second contract with SpaceX) is a massive technical milestone. These products deliver world-leading power levels, unlocking space ground station opportunities previously unattainable with solid-state solutions.

SpaceX Warrant Vesting & Starlink Momentum: SpaceX holds warrants for up to 15% of Filtronic’s share capital. As of early 2026, significant tranches have vested following $60M+ in orders. Any news regarding a Starlink IPO in 2026 would likely act as a major valuation proxy for Filtronic, given its “SpaceX-validated” status.

Sedgefield Operating Leverage: Investors are monitoring for “operating leverage” as the high fixed costs of the move are absorbed by the record H2 backlog, potentially driving a re-rating of EBITDA margins toward 2027.

UK Defense “Sovereign” Push: With the UK Ministry of Defence prioritizing domestic supply chains in 2026, Filtronic’s status as a secure, automated UK manufacturer makes it a primary candidate for upcoming electronic warfare and radar sensor contracts beyond its current £13.4M defense prime agreement.

B. Headwinds

Customer Concentration Risk: Despite successful diversification, SpaceX accounted for over 80% of turnover in the prior year. Any shift in SpaceX’s procurement strategy or a move toward vertical integration of RF hardware would significantly impact the revenue floor.

Investment-Phase Margin Compression: For FY2026, EBITDA is forecast at £10.9M (down from £17.0M in FY2025). This “planned” dip reflects a 29% increase in headcount and R&D. If the conversion of the order book into revenue hits technical delays, the high P/E ratio (approx. 60x) leaves the stock vulnerable to a pullback.

Currency Sensitivity (USD/GBP): Filtronic reports in Sterling but earns heavily in US Dollars. Continued strength in the Pound against a weakening Greenback through 2026 could create optical misses in top-line revenue reporting despite strong underlying volumes.

Talent Acquisition War: The demand for RF and mmWave engineers in the UK is at an all-time high. Filtronic’s ability to scale depends on retaining its core engineering team; any loss of key IP talent to larger aerospace incumbents could slow its technology roadmap for W-band and 6G development.

IV. SWOT Analysis

A. Strengths

Sedgefield Automated Manufacturing Moat: With the February 2026 opening of its new headquarters at NETPark, Filtronic has doubled its footprint and implemented high-volume automated microelectronics assembly. This facility allows the company to transition “turn-key” designs to mass production (TRL 6 to 9) with a level of repeatability and precision in mmWave frequencies that competitors may struggle to achieve at scale.

The “SpaceX-Validated” Status: Holding a multi-year partnership and a 15% warrant structure with SpaceX, Filtronic is the primary provider of E-band Solid State Power Amplifiers (SSPAs) for the Starlink constellation. This relationship provides not only a record £55.5M revenue floor for FY2026 but also a “global gold standard” validation that attracts other LEO constellation operators.

Sovereign RF Technical Leadership: Filtronic is a leader in GaN-on-SiC (Gallium Nitride on Silicon Carbide) technology, producing proprietary high-frequency amplifiers that offer superior power density and heat dissipation. Its ability to provide “Made in Britain” sovereign RF solutions makes it a non-displaceable partner for UK and European defense primes in electronic warfare and secure communications.

B. Weaknesses

Extreme Customer Concentration: Despite aggressive diversification, a significant majority of Filtronic’s backlog is tied to SpaceX and one or two European defense primes. Any shift in SpaceX’s internal vertical integration strategy or a delay in Starlink’s Gen3 rollout would have a disproportionate impact on the top line.

Investment-Phase Margin Compression: The heavy capital expenditure required for the Sedgefield move and a 29% headcount increase in late 2025 has led to a planned dip in EBITDA (projected £10.9M for FY2026 vs £17.0M in FY2025). This “digestive” period makes the stock’s high P/E ratio (approx. 48x) sensitive to any execution hiccups.

USD/GBP Currency Exposure: Filtronic reports in Sterling but earns a vast majority of its satellite revenue in US Dollars. The current 2026 weakness of the USD against the Pound acts as a persistent headwind, requiring the company to achieve higher unit volumes just to maintain flat “optical” revenue growth.

C. Opportunities

W-Band & 550W Ka-Band Expansion: Through NSIP funding awarded in late 2025, Filtronic is developing next-generation 550W Ka-Band SSPAs. This technology is designed to replace aging Traveling Wave Tube Amplifiers (TWTAs) in ground stations globally, opening a multi-billion dollar hardware replacement cycle.

6G & Terrestrial Backhaul: As 5G Advanced and early 6G standards emerge in 2026, the demand for E-band and W-band backhaul to handle massive data traffic is surging. Filtronic’s terrestrial telecoms heritage positions it to capture the infrastructure spend required for ultra-high-speed urban data links.

Expansion into “Direct-to-Device” (D2D): As satellite-to-phone connectivity becomes a standard feature, Filtronic’s ability to miniaturize high-frequency RF components for satellite payloads represents a massive incremental TAM in the emerging Non-Terrestrial Network (NTN) market.

D. Threats

SpaceX Vertical Integration: The greatest long-term threat is SpaceX (or other LEO giants) deciding to bring RF design and SSPA manufacturing entirely in-house. While the 15% warrant deal aligns their interests, any change in Elon Musk’s “Buy vs. Build” philosophy could evaporate the core backlog.

Global RF Engineering Talent War: The specialized skills required for mmWave engineering (30GHz+) are in critically short supply. Larger aerospace giants like Northrop Grumman or Lockheed Martin could use their superior capital to poach Filtronic’s core IP talent, stalling the 2026 product roadmap.

Geopolitical Supply Chain Shocks: Filtronic relies on specialized semiconductor wafers and rare materials for its GaN products. Renewed trade tensions or export controls on high-performance electronics could disrupt production timelines at the Sedgefield facility.

V. Price Targets

A. Near-Term Support & Consolidation (0–6 Months): GBX 260.00 – 295.00

The stock has successfully cleared the 250p psychological barrier following the February 3, 2026, Interim Report, which confirmed that the Sedgefield facility is now operating at peak efficiency.

Support Floor Maintenance: The previous resistance zone of 205p–215p has been definitively broken. Short-term support is now anchored at the 260p level, provided that H2 revenue delivery remains on track for the £55.5M+ target.

Margin Reclamation: Investors are now pricing in a “V-shaped” margin recovery. With the heavy lifting of the Sedgefield move complete, the market expects EBITDA margins to rebound toward 22% by year-end (May 31), justifying the current premium valuation.

B. Medium-Term Expansion (6–18 Months): GBX 310.00 – 350.00

To sustain a >300p valuation, Filtronic needs to prove its high-power GaN (Gallium Nitride) technology is the “gold standard” for the next generation of LEO satellite constellations.

The “Kuiper/Telesat” Catalyst: While SpaceX remains the anchor, securing a secondary Tier-1 satellite partner would likely trigger another leg up. A contract win with Amazon Kuiper would de-risk the “customer concentration” narrative and move the stock toward the 350p mark.

Warrant Dynamics: As of 2026, a portion of the 15% SpaceX warrants has vested. Clear communication regarding SpaceX’s intent to exercise (rather than just hold) these warrants would serve as a powerful institutional signal, effectively putting a “Musk Floor” under the share price.

C. Long-Term “Global Standard” Scenario (2027+): GBX 420.00+

The “Blue Sky” scenario assumes Filtronic transitions from a specialized supplier to the primary mmWave hardware architect for Western sovereign defense.

Standardization of E-Band: If Filtronic’s proprietary GaN SSPAs become the industry standard for ground stations globally, the company enters a high-margin, recurring revenue phase.

M&A Premium: At a market cap approaching £650M–£750M, Filtronic becomes a high-priority acquisition target for defense giants like BAE Systems or Northrop Grumman, who may pay a significant premium to secure “sovereign engineering” capabilities in the mmWave spectrum.

VI. Summary & “Go/No-Go” Signals

To evaluate whether to hold or increase a position in Filtronic (FTC), monitor these specific technical and operational triggers:

Accumulation Zone (The “Dip”): GBX 245.00 – 260.00 remains the ideal re-entry point. Any macro-driven pullback to these levels could be viewed as a buying opportunity, given the strength of the current order book.

The “Utilization” Watch: A vital signal is the Sedgefield Throughput. If the facility maintains high-volume delivery of the $62.5M SpaceX GaN order without quality-control delays, the “Go” signal for a long-term hold remains active.

Backlog Quality: Watch for the Defense-to-Space Ratio. A healthy signal is the defense segment (currently bolstered by the £13.4M sensor deal) growing to represent 30% of the total backlog, providing a counter-cyclical hedge to the more volatile satellite market.

Warrant Exercise: Monitor RNS announcements for any SpaceX warrant exercises. While dilutive, an exercise at the current price would be a massive vote of confidence, signaling that SpaceX sees significantly more upside beyond current price.