Insuring LEO Assets [Concept]

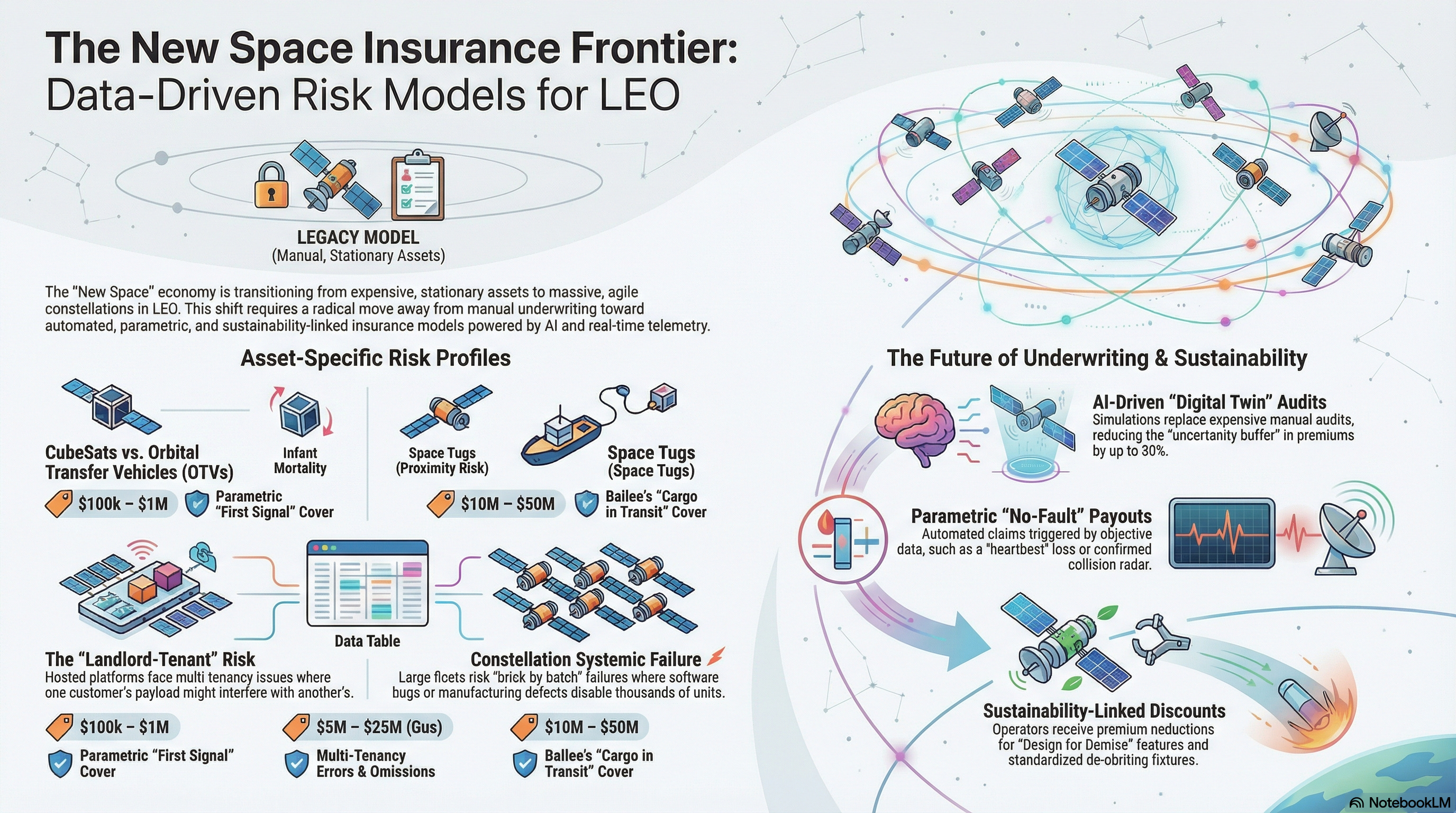

Low Earth Orbit (LEO) insurance needs to undergo a radical shift as the “New Space” economy moves from billion-dollar geostationary (GEO) assets to massive, agile constellations.

Low Earth Orbit (LEO) insurance needs to undergo a radical shift as the “New Space” economy moves from billion-dollar geostationary (GEO) assets to massive, agile constellations.

Innovation in this sector is evolving from traditional indemnity towards data-driven, parametric, and sustainability-linked models.

I. Asset-Specific Policy Frameworks

Traditional LEO insurance is often an afterthought. New policies could be segmented by the asset’s “behavioral” risk and physical profile.

1. CubeSats & NanoSats (Academic, R&D, & Rapid Imaging)

Small, cheap, and often built with “Commercial Off-the-Shelf” (COTS) parts, these assets have the highest failure rates in the industry.

Est. Asset Value: $100k – $1M per unit.

Risk Profile:

Infant Mortality: A high percentage of these assets may never “wake up” after deployment.

Limited Maneuverability: Many lack propulsion, making them “dumb” assets that cannot dodge debris, making them a liability to others.

Short Lifespans: High atmospheric drag at lower LEO altitudes means these are essentially “consumable” assets.

Example Insurance Opportunities:

Parametric “First Signal” Cover: $15,000 – $40,000 per launch. A one-time fee that pays out the full asset value if no “heartbeat” is detected within 48 hours of deployment.

Third-Party Liability (TPL): $5,000 – $15,000 annually. Standard $10M–$50M coverage limit for “space-to-space” collision liability.

Subscription-Based In-Orbit: $1,500 – $3,000 per month. Covers hardware failure; can be toggled off once mission data objectives are met.

2. Hosted Platform Providers (Space-as-a-Service)

These providers host multiple third-party payloads (sensors, cameras, or transponders) on a single bus. This creates a complex “landlord-tenant” risk dynamic that traditional “single-owner” policies cannot handle.

Est. Asset Value: $5M – $25M (Bus) + $1M – $5M per payload.

Risk Profile

Inter-Payload Interference: A “noisy” electronic payload from Tenant A may jam the sensitive sensor of Tenant B. The provider is often stuck in the middle of the liability claim.

“Common Carrier” Vulnerability: If the main bus power system fails, five or six different companies lose their primary mission simultaneously, leading to aggregated claims against the provider.

Resource Contention: If the platform has a partial power failure, the provider must “load shed.” Deciding which customer stays powered on and which gets shut down creates a massive breach-of-contract risk.

Data Sovereignty & Cybersecurity: Since multiple customers share the same downlink, a cyber-breach on one payload could potentially “pivot” to compromise the host or other payloads.

Example Insurance Opportunities

Multi-Tenancy E&O (Errors & Omissions): $80,000 – $150,000 annually. Protects the provider against tenant lawsuits for “resource contention” or “intentional load shedding” during power anomalies.

SLA Parametric Policy: $50,000 annually. Pays tenants $10k/day for every day (up to predefined limit) the host fails to meet the “Contracted Up-time” (Power/Data).

Cyber-Aggregation Rider: $20,000 – $40,000. Added to the base policy to cover forensic costs if a “tenant” payload compromises the host’s flight software.

3. Orbital Transfer Vehicles (OTVs) & Space Tugs

These are the “last-mile” delivery trucks of space. They are inherently risky because they are designed to move and interact with other objects.

Est. Asset Value: $10M – $50M.

Risk Profile:

Proximity Operations (ProxOps): The risk of “fender benders” during the release of payloads.

Propulsion Malfunction: If a tug’s engine hangs open, it becomes a high-velocity projectile across multiple orbital planes.

Multi-Client Liability: A single OTV may carry 20 different satellites from 20 different owners. A failure of the tug leads to a massive, multi-party legal entanglement.

Example Insurance Opportunities:

Bailee’s “Cargo in Transit” Cover: $200,000 – $500,000 per mission. Similar to marine cargo insurance; covers the OTV for the value of the 3rd party satellites it is carrying.

“Surge” Pricing for Docking: $10,000 per maneuver. A dynamic premium applied only during the 24-hour window of a payload release or docking attempt.

COLA (Collision Avoidance) Discount: 15–25% premium reduction for operators who prove 99.9% uptime of an automated collision avoidance system integrated with 3rd-party tracking data.

4. Constellations (Broadband & Global Sensing)

These assets operate on a philosophy of “redundancy through numbers.” The failure of a single unit is expected and statistically irrelevant to the business model.

Asset Valuation: $500M – $5B+ (Total Fleet).

Risk Profile:

Systemic Failure: A batch-wide manufacturing defect or a software bug pushed via update that “bricks” thousands of units simultaneously.

Regulatory Non-Compliance: If a constellation fails to meet de-orbiting timelines, it faces fines or loss of operating licenses.

Collision Cascades: The “Kessler Syndrome” risk is highest here; one fragmentation event can disable a whole orbital shell.

Example Insurance Opportunities:

Revenue-at-Risk (Net Availability): $1M – $5M annual premium. $50M+ payout limit. Triggered only if the total fleet capacity drops below a critical threshold (e.g., 92% availability).

De-orbiting Performance Bond: $500 – $2,000 per satellite. Funds are held in escrow/insurance to pay for “Active Debris Removal” (ADR) if the satellite dies before it can self-deorbit.

Portfolio Blanket Cover: $500k – $2M annually. Covers the “top 5%” of assets that fail due to non-standard causes (e.g., a specific debris-heavy orbital shell).

5. In-Orbit Servicing & Manufacturing (IOSM)

This category includes robotic arms for repair, refueling stations, and “space factories” growing crystals or tissues.

Asset Valuation: $50M – $200M (Servicer); High variable (Product).

Risk Profile:

Mechanical Interaction Failure: The risk that a robotic gripper damages a sensitive solar array during a repair attempt.

Chemical Contamination: For refueling missions, the risk of hypergolic fuel leaks damaging the “client” satellite’s sensors.

Product Liability in Orbit: If a “space-made” pharmaceutical is corrupted because of a micro-vibration in the station, who is liable?

Example Insurance Opportunities:

Orbital Malpractice Insurance: $300,000 – $750,000 annually. Covers the servicer for damage caused to the “client” satellite during refueling or repair.

Product Liability (Space-Made): $50,000 – $150,000 per batch. Covers the loss of value for pharmaceuticals or semiconductors grown in orbit if the station fails to maintain “microgravity purity.”

Contact-Induced Loss (CILOL): 2–5% of the Client Asset Value. A short-term policy taken out by the client to ensure they are paid if the servicing mission accidentally destroys their satellite.

II. Leveraging Technology for Reducing Insurance Costs

The “soft costs” (underwriting hours, legal fees) and “hard costs” (claims adjustment, data acquisition) currently make LEO insurance potentially prohibitive for small operators.

By moving away from manual “expert-opinion” underwriting and toward automated, high-fidelity data streams, the industry could reduce both soft costs (labor and administration) and hard costs (loss adjustment and data procurement).

1. AI-Driven Underwriting (Reducing Soft Costs)

Legal review, technical auditing, and manual risk modeling (soft costs) may traditionally account for up to 30–40% of the premium for small-to-midsize LEO missions.

“Digital Twin” Simulations:

The Mechanism: Underwriters require a high-fidelity digital twin of the asset to run millions of Monte Carlo simulations against a live debris catalog and dynamic space weather models. This virtual replica tests the satellite’s shielding and electrical architecture against simulated solar flares, radiation flux, and increased atmospheric drag caused by solar activity.

Cost/Risk Impact: This replaces the $25k+ specialized engineering audit. By proving a satellite’s “collision avoidance burden” and space weather resilience profile are high through simulation, an insurer can lower the “uncertainty buffer” in the premium by 20–30%, as the AI quantifies exactly how the asset will handle a 1-in-100-year solar event..

Automated Orbital Credit Scoring:

The Mechanism: Machine Learning models ingest flight heritage data for specific bus components (e.g., an X-brand reaction wheel).

Cost/Risk Impact: Similar to a consumer credit score, this creates an “Orbital Risk Index.” Standardized missions (like a 3U CubeSat using 100% flight-proven parts) can receive an instant quote via API, reducing the “time-to-quote” from 4 weeks to 4 minutes and cutting administrative overhead by 70%.

Generative AI Policy Personalization:

The Mechanism: Large Language Models (LLMs) draft policy wordings that are “orbit-aware.” If a mission is at 550km (high drag) vs. 400km (low drag), the AI automatically adjusts the “End-of-Life” (EoL) clauses.

Cost/Risk Impact: This eliminates the need for 40+ hours of expensive specialized legal counsel ($500+/hr). It ensures that the legal language perfectly matches the physical reality of the mission, reducing “coverage gap” litigation.

2. IoT & Real-Time Telemetry (Reducing Hard Costs)

Hard costs include the expensive process of forensic claims adjustment; proving why a satellite failed when it is 500km overhead.

“Black Box” Underwriting & Claims:

The Mechanism: Satellites equipped with “Insurance-Grade” telemetry modules send cryptographically signed health data (power, thermal, CPU) to a secure insurer vault.

Cost/Risk Impact: In the event of a failure, the data serves as Proof of Loss. This removes the need for an “Adjustment Committee” which can cost upwards of $100,000 per claim in technical consulting fees.

Space Situational Awareness (SSA) Integration:

The Mechanism: Direct API feeds from providers like LeoLabs or Slingshot Aerospace are integrated into the policy.

Cost/Risk Impact: If a satellite enters a “High Density Debris Shell,” the premium adjusts dynamically (Usage-Based Insurance). This lowers the insurer’s “tail risk” by incentivizing operators to stay in safer, less-congested orbits to save money.

3. Parametric "No-Fault" Payouts (Reducing Claims Processing)

By using objective, third-party data as a “trigger,” insurers could eliminate the subjective, months-long loss-adjustment process, providing immediate liquidity to operators.

A. Silent Satellite (Communication Failure)

This trigger addresses the “brick in the sky” scenario where an asset simply ceases to transmit, often due to an internal power failure or processor “latch-up.”

The Technical Verification:

Verification is handled by independent ground station networks (e.g., KSAT, Atlas, or LeafSpace).

The policy triggers if these global networks fail to receive a “heartbeat” or telemetry packet for a continuous period; typically >72 hours.

The data is cryptographically signed by the ground station provider and pushed to the insurer’s smart contract.

Insurer Cost & Risk Reduction:

90% Administrative Reduction: Traditional claims require a forensic engineering team to analyze “last known telemetry” to prove the failure wasn’t due to an excluded cause (like a software update error). Parametric “No-Fault” skips this.

Elimination of Legal Disputes: There is no debate over why it happened. If the signal is gone, the check is cut.

B. Conjunction Event (Confirmed Collision)

Collision with untracked debris is a “Force Majeure” event that is notoriously difficult to distinguish from internal mechanical failure without this specific trigger.

The Technical Verification:

Relies on Space Situational Awareness (SSA) radar and optical data from providers like LeoLabs or Slingshot Aerospace.

The trigger is activated when a “Fragmentation Event” is detected at the asset’s specific Two-Line Element (TLE) coordinates, or if the radar cross-section (RCS) of the asset suddenly changes in a way that indicates a breakup.

Insurer Cost & Risk Reduction:

100% Forensic Savings: In traditional insurance, the “did it break or was it hit?” argument can be time consuming. SSA data provides a definitive “Yes/No” on external impact.

Basis Risk Mitigation: By tying the payout to a verified radar hit, the insurer avoids paying for manufacturing defects hidden under the guise of “unknown orbital impact.”

C. Service Level Agreement (SLA) Power/Performance Drop

This is a “partial loss” trigger, essential for Hosted Platforms or Communication Constellations where the satellite is still alive but no longer commercially viable.

The Technical Verification:

Uses on-board, immutable IoT sensors that report directly to the insurer via an encrypted secondary “out-of-band” link.

The trigger is met if the bus provides <50% of nominal power (or a drop in data throughput) for a sustained period, such as 5 consecutive orbits.

Insurer Cost & Risk Reduction:

Replacement of Revenue Audits: In traditional “Loss of Revenue” claims, adjusters must spend months auditing the operator’s books to calculate lost profit.

Fixed-Fee Payouts: The parametric policy pays a pre-agreed “flat fee” based on the performance drop. This turns a complex variable liability into a predictable, binary expense for the insurer.

III. Alternative Underwriting & Risk Transfer

The LEO insurance market could beyond traditional “broker-and-underwriter” negotiations toward decentralized, automated, and sustainability-aligned structures. These models could increase capital capacity while dramatically lowering the cost of entry for Smallsat operators.

1. Peer-to-Peer (P2P) Risk Pools & Mutuals

The traditional insurance market may lack the appetite for high-frequency Smallsat risks. P2P models could allow the industry to self-insure “the first dollar” of loss.

Constellation Co-ops (Protection & Indemnity Mutuals):

The Mechanism: Inspired by maritime P&I Clubs, groups of LEO operators form a mutual pool. Each member contributes a “call” (premium) based on their fleet’s risk score.

Operational Detail: If a member suffers a loss, the pool pays out from its shared reserves. Because members “own” the pool, there is a massive incentive for mutual peer-review of engineering standards, which naturally lowers the risk of the entire group.

Capacity Benefit: This handles high-frequency, low-severity losses (e.g., single CubeSat failures), leaving traditional commercial insurers to only cover “excess of loss” for catastrophic events like a major collision.

Mutual Risk Sharing Communities:

The Mechanism: Smaller operators (universities, startups) contribute to an AI-managed “Captive” pool.

The Deep Detail: The AI monitors live telemetry across all pool members. If the pool maintains a high safety rating, members receive a “dividend” or premium credit. This turns insurance from a sunk cost into a performance-linked asset.

2. Tokenized Risk & Space Bonds

By converting orbital risk into a digital asset, the space industry can tap into global capital markets, bypassing the capacity limits of the traditional Lloyd’s of London market.

Space Debris Insurance Bonds (SPADRIBs):

The Mechanism: These are “Catastrophe Bonds” for space. An operator issues a bond to investors. If the mission is successful, investors receive high-interest coupons (the “premium”). If a “trigger event” occurs (e.g., a satellite becomes debris), the principal is used to pay for the loss or a removal mission.

Tokenized “Fractional” Risk:

The Mechanism: Risk is sliced into thousands of digital tokens on a blockchain. Retail or institutional investors can buy tokens representing a specific mission’s risk.

Administrative Impact: This democratizes space investment. A Smallsat operator can “crowdsource” their insurance capital, paying investors a yield that is often lower than the high margins demanded by traditional space insurers.

3. On-Chain Parametrics & Smart Contracts

By encoding the policy into a smart contract, the need for human administration is reduced.

Oracle-Driven Execution:

The Mechanism: A Smart Contract “listens” to a trusted Data Oracle (e.g., Space-Track.org or LeoLabs).

Automatic Payout: If the Oracle confirms an object has “Decayed” (fallen out of orbit prematurely) or has been involved in a “Conjunction” (collision), the smart contract instantly releases the claim payment to the operator’s digital wallet.

Cost Reduction: There are no claims forms, no lawyers, and no adjustment fees. This could reduce “Soft Costs” from 15% of the premium to <1%.

IV. Sustainability-Linked Policies (ESG)

The “monetization of sustainability” could transform space debris mitigation from a regulatory burden into a tangible financial asset. A satellite’s Sustainability Score could become as critical to its bankability as its technical specifications.

1. End-of-Life (EoL) Performance Bonds

The UK Space Agency and other regulators could begin integrating these bonds into the licensing process.

The Mechanism: The “Orbital Security Deposit”

At launch, the operator places a De-orbiting Deposit (typically 5–8% of total mission cost) into an interest-bearing, ring-fenced bond.

These bonds could be tradeable; an operator can sell the bond to a third party, effectively transferring the “cleanup obligation” along with the asset’s ownership.

The Payout Logic:

Success (The “Green Return”): If the operator successfully de-orbits the satellite at the end of its useful life, the bond is released back to them with accrued interest. This interest often offsets a portion of the original insurance premium.

Failure (The “Automated Cleanup”): If the satellite becomes non-responsive (a “Zombie”), the bond is forfeited. The capital is automatically diverted via a Smart Contract to pre-approved Active Debris Removal (ADR) providers like Astroscale or ClearSpace.

Financial Impact: This could guarantee that the cost of cleanup is “pre-funded,” removing the liability from the public taxpayer and ensuring the “polluter pays” principle is physically enforced by capital.

2. Sustainability-Linked Variable Liability (SLVL)

Insurers could offer a sliding scale for Third-Party Liability (TPL) requirements based on the “Design for Demise” and “Design for Removal” characteristics of the asset.

Variable Liability Limits:

Regulators traditionally required a flat €60M–€100M TPL cover. “Sustainable” satellites could see these mandates drop to as low as €20M, drastically reducing the “Premium Hard Cost.”

Specific Discount Tiers:

Passive De-orbiting (Drag Sails/Terminator Tapes): Assets equipped with “fail-safe” passive systems that ensure reentry even without power receive an immediate 10–12% premium discount.

Standardized Grappling Fixtures: Satellites designed with magnetic docking plates or robotic “handshakes” (like the Astroscale Proximity Operations standard) receive a 15% discount. This is because they are “insurance-friendly”; if they break, they are easy to fix or remove.

Green Propellant Incentives: Replacing toxic Hydrazine with high-performance, non-toxic alternatives (like LMP-103S) reduces the “Environmental Impairment” risk. This allows insurers to offer “Clean Orbit” credits, further lowering the annual liability premium by 5–8%.

3. ESG-Rated Underwriting & “Space Bonds”

As institutional investors (ESG funds) move into the space sector, they may demand “Space Sustainability Ratings” (SSR) as a condition for investment.

The ESG Multiplier: A high SSR score (validated by AI-driven digital twin audits) could reduce the “Uncertainty Buffer” in a policy by up to 25%.

Direct Venture Benefit: Startups with “Sustainability-Linked Policies” could see higher valuations. Insurance could be viewed as a safety signal to VCs that the company is “future-proofed” against upcoming orbital debris taxes.