ispace ($9348.T) [Investing]

Institutional investors are balancing the company’s technical progress (achieving stable lunar orbit) against the persistent “execution risk” of landing and a high cash-burn rate.

ispace is a global lunar exploration company with a vision to create a sustainable “Cislunar economy” by 2040. The company’s core business model is centered on providing high-frequency, low-cost access to the Moon through three primary integrated services.

1. Payload Services (Lunar Logistics)

ispace’s flagship offering is a “last-mile” transportation service for cargo (payloads) to the lunar surface and orbit. They utilize a tiered lander architecture to meet varying mission requirements:

Series 1 (HAKUTO-R): A compact, small-scale lander used for the initial Mission 1 and Mission 2 (RESILIENCE). It is designed to carry approximately 30kg of cargo, acting as a secondary payload on rockets like the SpaceX Falcon 9.

Series 3 (APEX 1.0): Developed primarily by ispace-U.S., this is a larger, high-performance lander with a 500kg payload capacity. It is the cornerstone of ispace’s participation in NASA’s Commercial Lunar Payload Services (CLPS) program, capable of reaching the lunar far side.

Surface Mobility: In tandem with landers, ispace develops micro-rovers like TENACIOUS (designed by its Luxembourg office) to provide mobility, sample collection, and regolith extraction services on the lunar surface.

2. Lunar Data Services

Recognizing that physical transport is only half the equation, ispace is building a high-margin data ecosystem. This service involves collecting, analyzing, and selling vital lunar environmental data to government agencies and private firms.

Telemetry & Imagery: Selling high-definition video and technical telemetry captured during lunar descent and orbital operations.

Resource Mapping: Identifying the location and concentration of water ice and minerals (such as Helium-3) to assist future mining and habitat-building missions.

Communications Relay: Utilizing its own relay satellites (Alpine and Lupine) to provide data transfer for customers operating on the lunar far side where direct Earth communication is blocked.

3. Space Resource Development & Partnerships

This segment focuses on the long-term goal of harvesting lunar resources to sustain human life and fuel further space travel.

Water Ice Harvesting: Strategic partnerships with industrial firms like Kurita Water Industries and Takasago Thermal Engineering to develop water treatment, electrolysis, and hydrogen fuel production on the Moon.

Partnership Program: ispace offers a collaborative “Marketing & R&D” package where companies can use ispace’s mission activities for branding, technical validation of their products in extreme environments, and corporate social responsibility (CSR) initiatives.

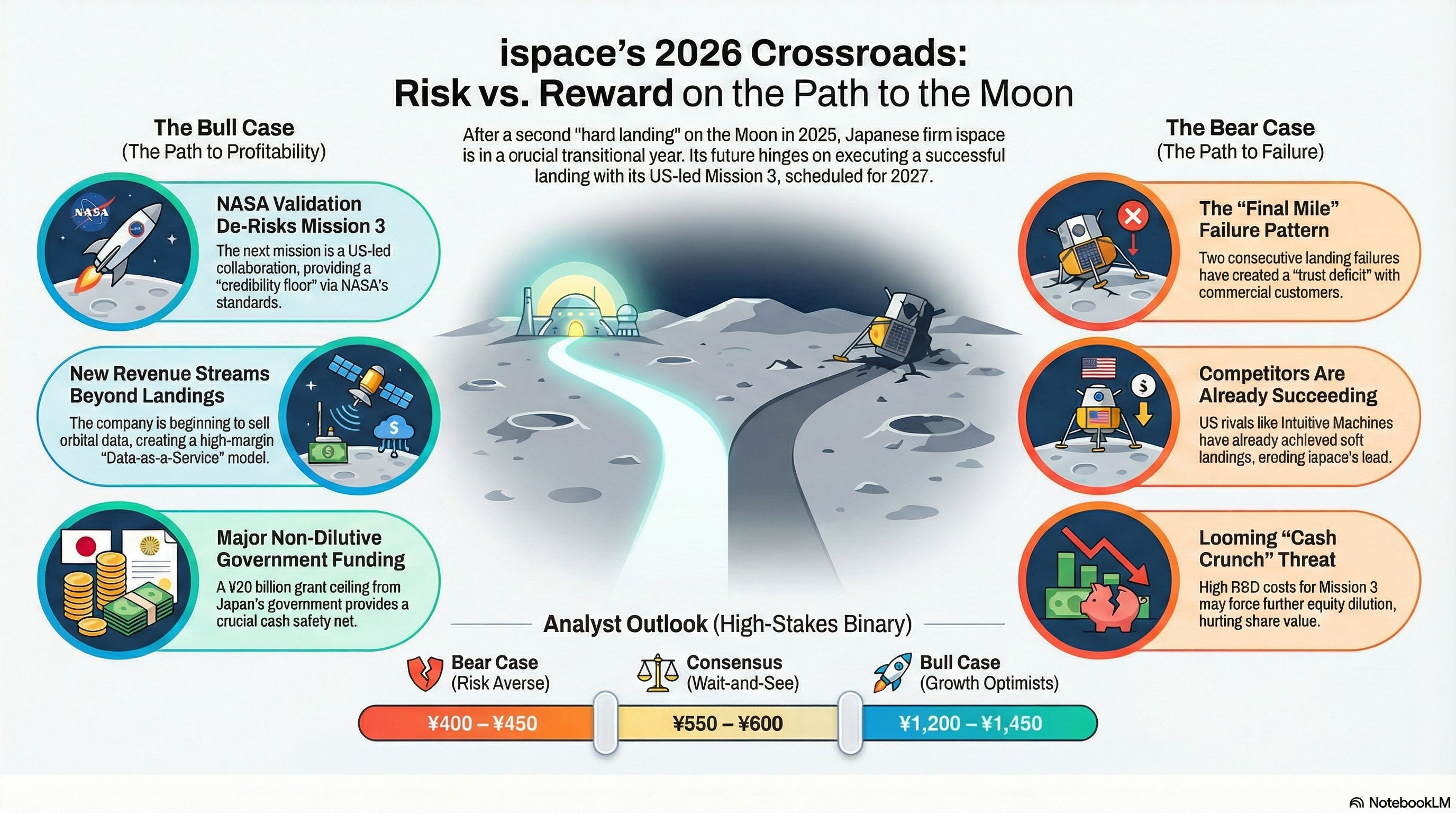

I. Market & Analyst Sentiment

Institutional investors are balancing the company’s technical progress (achieving stable lunar orbit) against the persistent “execution risk” of landing and a high cash-burn rate.

A. The Bull Case: ¥1,200–¥1,450 (Growth Optimists)

The most optimistic outlooks view the recent “hard landing” as a valuable data-gathering exercise that de-risks the upcoming U.S.-led Mission 3.

The “Data as Asset” Narrative: Bulls argue that ispace has now successfully navigated the transit and orbital insertion phases twice. They view the identified “laser rangefinder” glitch as a solvable hardware fix rather than a systemic failure of the flight software or propulsion.

NASA CLPS Validation: The bull case rests heavily on the APEX 1.0 lander, which is being developed in the U.S. in collaboration with Draper. Analysts in this camp believe the shift to a U.S.-based supply chain for Mission 3 provides a “credibility floor” backed by NASA’s lunar architecture requirements.

Expanding Payload Ecosystem: Recent agreements, such as the January 2026 deal with Dymon for payload transportation boxes, signal a move toward a “standardized shipping” model for the Moon, which bulls believe will lead to higher-margin, recurring service revenue.

B. The Consensus View: ¥550–¥600 (Wait-and-See)

The consensus reflects a “Buy/Hold” stance, acknowledging the company’s leadership in the commercial lunar market but wary of the extended timeline to Mission 3.

The 2027 Timeline Gap: With the next landing attempt pushed to 2027, the consensus is that the stock may remain range-bound in 2026. Analysts are looking for “Success 9” (landing) as the only catalyst capable of a permanent valuation re-rating.

Revenue vs. Burn: While revenue is growing (projected to increase by ~31% for FY2026), the company continues to post net losses (approx. ¥2.8 billion in recent quarters). Analysts are closely monitoring ispace’s ability to secure non-dilutive funding or government grants to bridge the two-year gap between missions.

C. The Bear Case: ¥400–¥450 (Risk Averse)

Bears focus on the competitive landscape and the fragility of the “lunar economy” business model.

“Binary Outcome” Risk: Bears argue that ispace is a “zero or one” stock. Two consecutive landing failures have created a “trust deficit” that makes it harder to attract commercial (non-government) payload customers who require high mission assurance.

Institutional Fatigue: With the stock underperforming the broader JP Aerospace & Defense industry (which returned 72% in 2025 vs. ispace’s negative return), bears fear institutional investors will rotate capital toward profitable defense incumbents rather than speculative space startups.

The “Cash Crunch” Threat: Given the high costs of the Series 3 lander design, bears remain skeptical of the current balance sheet. They anticipate further equity dilution in mid-2026 to fund the heavy R&D required for Missions 3 and 6.

II. Financial Health & Strategic Resilience (Q1 2026)

Following the “Mission 2” lunar landing attempt in mid-2025, ispace’s financial strategy has shifted from pure R&D toward building a stable, multi-mission capital structure. While the company remains in a pre-profitability growth phase, its focus for early 2026 is on leveraging Japanese government subsidies and recent equity raises to bridge the gap to Mission 3.

1. Cash Runway & Burn Management

Liquidity Position: As of January 2026, ispace maintains a cash and equity reserve of approximately ¥20.1 billion (approx. $135M USD). This follows a major ¥18.2 billion capital raise completed in late 2025 via third-party allotments and new share issuances designed to fund the heavy development cycles for Missions 3 and 4.

Burn Rate & Funding Efficiency: The company is currently “burning” cash at a rate commensurate with the development of the high-capacity APEX 1.0 lander. However, the burn is increasingly offset by non-dilutive funding, including a ¥20 billion grant ceiling from Japan’s “Space Strategy Fund” which provides a multi-year safety net for high-precision landing tech.

Path to FCF Positivity: Analysts do not expect positive Free Cash Flow (FCF) until FY2028/29, following the successful execution of Mission 3. The current priority is “Mission Success” over “Margin Expansion,” with management focusing on maintaining at least 18–24 months of runway at all times to avoid “distress” financing.

2. Backlog Quality and Phasing

Backlog Composition: ispace’s backlog is diversifying beyond “symbolic” payloads toward commercial resource prospecting. A landmark $22 million contract with Magna Petra (announced Nov 2025) for Helium-3 prospecting on Mission 3 highlights a shift toward higher-value scientific and industrial customers.

Government Anchor Contracts: The financial backbone is supported by the NASA CLPS (Task Order CP-12) and the Japanese government’s “Stardust” program. These contracts provide milestone-based payments that de-risk the R&D costs of the lander’s propulsion and guidance systems.

Revenue Recognition: For FY2026 (ending March 2026), ispace has guided for an approximate 31% increase in net sales. Notably, the company recognized its first “Lunar Data” sales revenue in late 2025, signaling the start of a high-margin data-as-a-service (DaaS) business model.

3. Capex to Revenue Intensity

Peak Development Cycle: ispace is currently in a secondary peak investment phase. While “Mission 2” hardware costs are retired, CapEx is redirected toward the M3 and M6 landers, which are significantly larger and more complex. Development of the Series 3 lander for polar missions remains the primary capital driver.

Strategic Leverage: The debt-to-equity ratio remains a point of scrutiny for the bears (recently cited at high levels due to venture debt), but the company has successfully secured ¥10 billion+ in loan support from major Japanese banks like SMBC, suggesting strong institutional backing from the domestic financial sector.

Margin Evolution: While currently reporting net losses (approx. ¥27.21 loss per share in recent quarters), “Project Income” - a metric ispace uses to show gross profit on specific missions - is projected to nearly double by 2027 as payload capacity increases and launch costs are shared across more customers.

III. 2026 Catalysts to Monitor

A. Tailwinds

Mission 3 “Maturity” Re-Rating: Following the technical post-mortem of the June 2025 hard landing, ispace is expected to complete the final design review of the APEX 1.0 lander in mid-2026. Evidence that the laser rangefinder latency issues have been architecturally resolved would de-risk the 2027 launch and serve as a primary catalyst for institutional “Buy” upgrades.

Japan Space Strategy Fund Inflows (¥20B Ceiling): In January 2026, ispace was selected for a massive government grant focused on “High Precision Landing Technology.” Investors are watching for the first tranche of this funding; unlike equity raises, this non-dilutive capital provides a significant cushion for the ¥2.8 billion quarterly burn without hurting share value.

Lunar Data Service Launch (Q3 2026): Management has signaled a shift toward selling telemetry and environmental data collected during Mission 2’s orbital phase. Establishing a “Data-as-a-Service” revenue stream in 2026 would prove the business model is not solely dependent on successful physical landings.

Expanding Payload Partnerships: The January 30, 2026, agreement with Dymon to develop a standardized “Lunar Transport Box” indicates the start of a logistics ecosystem. Similar contract wins throughout 2026 could see ispace’s backlog exceed ¥25 billion, providing better visibility into long-term cash flows.

B. Headwinds

The “Mission 3” Waiting Game: With the APEX 1.0 launch scheduled for 2027, 2026 risks becoming a “execution vacuum.” In the absence of a mission launch, the stock may suffer from retail investor fatigue and low trading volume, making it vulnerable to short-selling or negative sector rotations.

Competitive “First Mover” Erosion: Competitors like Intuitive Machines and Astrobotic are also targeting lunar far-side and polar missions in the 2026–2027 window. If a competitor achieves a “perfect” soft landing while ispace is in its two-year re-tooling phase, market share and “prestige” premiums could shift toward U.S. peers.

Liquidity & Dilution Risk: Despite the government grants, the high cost of the Series 3 lander development (for Mission 6) may necessitate a secondary offering in late 2026. Any further dilution could trigger the ¥400 Bear Case valuation.

Launch Vehicle Bottlenecks: While ispace is booked on SpaceX and potentially other providers, any broader industry delays in heavy-lift vehicle availability (e.g., Starship or Falcon Heavy schedules) could push the 2027 mission into 2028, further straining the company’s cash runway.

IV. SWOT Analysis

A. Strengths

Proven Orbital Navigation: ispace has successfully navigated to the Moon and entered stable lunar orbit twice (Mission 1 and Mission 2). This “Success 8” milestone proves that their flight software, deep-space communication (via SSC), and propulsion systems are battle-tested for the 380,000km transit.

Global Strategic Footprint: Unlike regional competitors, ispace operates through three distinct subsidiaries. ispace-US leads the NASA-backed Mission 3, while ispace-Europe focuses on rover robotics and mining. This allows the company to tap into multiple government funding pools (NASA CLPS, ESA, and Japan’s METI).

High-Value Payload Backlog: As of late 2025, ispace has secured a payload contract value of $86 million for Mission 3 alone. The inclusion of high-stakes commercial contracts, such as the $22 million Magna Petra Helium-3 agreement, signals that the market views ispace as a viable industrial partner.

B. Weaknesses

The “Final Mile” Failure Pattern: While orbit is a success, the company has yet to achieve a “soft landing.” This repeated failure at the landing phase creates a psychological barrier for conservative institutional investors and may lead to higher insurance premiums for future payloads.

Intense Capital Dilution: To fund the jump from the 1,000kg Series 2 lander to the massive Series 3 (APEX 1.0) lander, ispace has substantially diluted shareholders. The ¥18.2 billion raise in late 2025 was necessary but capped the near-term upside for early-stage investors.

Extended “Dark Periods” Between Launches: The decision to push Mission 3 to 2027 leaves a nearly two-year gap without a major mission launch. This lack of news flow often leads to share price stagnation as the market shifts focus toward competitors with more frequent launch cadences (e.g., Intuitive Machines).

C. Opportunities

Japan’s “Space Strategy Fund”: With a total ceiling of ¥20 billion available through JAXA/METI, ispace has a unique opportunity to fund its R&D through non-dilutive government grants. Capturing the full amount would drastically improve its cash flow profile without requiring new share issuances.

The “Lunar Data” Marketplace: By successfully transmitting telemetry and high-resolution imagery from lunar orbit during Mission 2, ispace recognized its first Data Sales Revenue in August 2025. This potentially creates a high-margin, scalable software-as-a-service (SaaS) model that isn’t dependent on physical cargo.

First-Mover Advantage in Resource Prospecting: Through its European subsidiary’s mass spectrometer development, ispace is positioning itself as the “pick and shovel” provider for the lunar mining industry (Helium-3 and Water Ice), a market projected to grow as the Artemis program matures.

D. Threats

Aggressive US Competition: Competitors like Intuitive Machines ($LUNR) have already demonstrated successful landings. If U.S. peers continue to stack successes while ispace is in a multi-year re-tooling phase, the “Commercial Lunar Lead” title could be permanently lost.

Launch Vehicle Dependency: ispace remains heavily reliant on SpaceX’s Falcon 9/Heavy. Any systemic grounding of the Falcon fleet or prioritization of NASA/Starlink missions could result in costly delays for the 2027 mission window.

Risk of a “Third Strike”: Market sentiment is currently forgiving of the “Success 8” (orbital) achievements. However, a third consecutive landing failure during Mission 3 (2027) could be an existential event, making it nearly impossible to raise further private capital.

V. Price Targets

A. Near-Term Resistance (0–6 Months): ¥550 – ¥680

The stock is currently recovering from its 2025 lows. In this window, ispace may trade primarily on liquidity preservation and non-dilutive grant news.

Grant Recognition & Liquidity Floor: Official approval and first disbursement of the ¥12 billion+ JAXA Strategic Fund tranches could provide a “liquidity floor” near ¥550. This non-dilutive capital is critical for investor confidence, as it reduces the immediate threat of another “dilution event” (equity raise) which has historically capped share price gains.

Q3 FY2026 Earnings (Feb 9, 2026): If the company confirms a narrower-than-expected loss due to its new Lunar Data revenue stream, it could break the ¥600 resistance level. Analysts are looking for a “Proof of Concept” in the services segment - specifically, high-margin sales of Mission 2 telemetry - to justify a shift away from a pure hardware-cost valuation.

Commercial Payload Momentum: Announcements of new, high-profile payloads for Mission 3 (APEX 1.0) would signal that the market “trusts” the new lander design. Securing a diversified mix of international commercial customers (beyond government agencies) during this window will be a key indicator of market resilience.

B. Medium-Term Consolidation (6–18 Months): ¥700 – ¥950

To reach this range, ispace must provide tangible proof that Mission 3 is on track for a flawless 2027 execution, moving past the “R&D struggle” phase.

Critical Design Review (CDR) & Hardware Freezing: Successful completion of all hardware testing for the APEX 1.0 lander in mid-2026 will serve as a massive technical de-risking event. Once the design is “frozen” for flight, the narrative shifts from “can they build it?” to “when do they launch?”; a transition that typically attracts more risk-averse institutional capital.

Payload Backlog Expansion & Revenue Visibility: Reaching a total backlog of $100M+ (¥15B+) would give analysts enough visibility to move the stock toward a ¥900 “Fair Value” target. A strong “book-to-bill” ratio in late 2026 would demonstrate that the company is successfully capturing the growing global demand for lunar logistics.

U.S. Subsidiary Performance (NASA CLPS): As Mission 3 is a U.S.-led mission (ispace-US), reaching key milestones in the NASA CLPS program will be pivotal. Success here integrates ispace into the NASA Artemis architecture, providing a “moat” of legitimacy that Japanese domestic competitors currently lack.

C. Long-Term “Success 9” Scenario (2027+): ¥1,400+

The “Blue Sky” scenario assumes a successful soft landing on the Lunar Far Side and the transition to a sustainable logistics utility.

Mission 3 Soft Landing (Schrödinger Basin): A successful touchdown would trigger a massive re-valuation, potentially returning the stock to its all-time highs. Achieving “Success 9” (landing) is the ultimate binary catalyst; it validates the lander’s GNC (Guidance, Navigation, and Control) systems and ends the “failure loop” that has haunted the stock since 2023.

Resource Prospecting & High-Margin Mining Data: Following a landing, the ability to sell on-site environmental and resource data (e.g., water ice or Helium-3 prospecting) transforms the company from a “carrier” into a “data provider.” This shift to a recurring-revenue model would allow ispace to command the higher multiples typically reserved for tech and SaaS companies.

Scale of the Series 3 Fleet: By 2027, if ispace successfully transitions to a multi-lander production line (M3 and M6), the economies of scale will begin to kick in. Demonstrating that the company can launch every 12–18 months at a declining cost per kilogram would solidify its position as the “FedEx of the Moon,” justifying a long-term premium valuation.

VI. Summary & “Go/No-Go” Signals

To evaluate whether to hold or accumulate ispace (9348.T) during the 2026 “transition year,” monitor these signals:

Accumulation Zone: ¥480 – ¥520 is the historical support zone where institutional buying has stepped in following technical setbacks.

The “Grant Watch”: A key signal of health is the ratio of Government Subsidies vs. Equity Financing. If the company can fund 2026 operations primarily through the Space Strategy Fund, it could be a strong “Buy” signal.

Competitive Execution: Watch the landing attempts of peers in 2026. If the “industry success rate” for lunar landings improves, the rising tide will likely lift ispace; however, continued industry-wide failures may cause a sector-wide “capital flight.”