Space-Based Quantum Internet [Innovation]

Early adopters are looking for Practical Quantum Advantage (PQA); quantum-enhanced workflows that delivers results that are either more accurate, more energy-efficient, or uniquely secure.

While established "Quantum Cloud" titans like IBM, Google, and Microsoft continue to dominate the high-level processing landscape, a frontier of the industry is shifting toward the enabling infrastructure.

A new generation of agile startups and specialized engineering firms is now building the essential hardware that makes a space-to-ground quantum link possible.

For innovators and strategic investors, the following sections detail considerations for significant growth opportunities in the emerging Quantum market.

I. Examples of Quantum Early Adopters

Early adopters are looking for Practical Quantum Advantage (PQA); the moment a quantum-enhanced workflow delivers a result that is either more accurate, more energy-efficient, or uniquely secure compared to classical methods.

1. The “Stage-Gate” Engagement Model

Directly selling a $50M system is rare. Instead, successful vendors appear to be using a phased approach to build the business case:

Phase 1: Opportunity Framing (The “Quantum Audit”): Identifying which 5% of a company’s classical workload is “quantum-ready.”

Phase 2: PoC & Benchmarking: Running small-scale experiments on NISQ (Noisy Intermediate-Scale Quantum) hardware or high-fidelity simulators to prove the algorithm works.

Phase 3: Hybrid Integration: Offloading specific sub-routines (like a chemical bond energy calculation) to a QPU while the rest of the stack remains on classical GPUs.

2. Industry-Specific Value Hooks

A. Automotive & Aerospace (“The Sustainability Multiplier”)

The Pitch: Sell quantum as the only viable way to meet Net-Zero 2040 targets.

BMW/Airbus Context: They are buying a reduction in R&D cycles. By simulating the Oxygen Reduction Reaction (ORR), they can bypass thousands of physical prototype failures for fuel cells.

Sales Strategy: Focus on “Materials Sovereignty.” If a competitor discovers a cobalt-free battery first via quantum simulation, they own the next decade of the EV market.

B. Pharmaceuticals (From Probabilistic to Deterministic Discovery”)

The Pitch: Moving away from the “fail fast” model to a “predict first” model.

Roche/Biogen Context: The focus is on Lead Optimization. Quantum nodes simulate how a drug binds to a protein at the sub-atomic level.

Sales Strategy: Use “Time-to-Market” as the primary KPI. A 20x speedup in chemical transformation simulations (as seen in the AstraZeneca/NVIDIA/IonQ pilots) translates to billions in extended patent life.

C. Finance & Logistics (“Precision vs. Probability”)

The Pitch: “In a volatile market, 1% more precision equals $100M in avoided risk.”

JPMorgan/HSBC Context: They are buying “Risk Mitigation.” Quantum Monte Carlo simulations can price complex derivatives with far fewer samples than classical methods.

Sales Strategy: Sell the “Quantum-Safe” Narrative. With “Harvest Now, Decrypt Later” threats looming, selling Quantum Key Distribution (QKD) is an easier entry to quantum than complex algorithm development.

II. Emerging Trends

This evolution is defined by three critical trends that are effectively building the “on-ramps” to a space-based quantum internet.

A. The Move to “Hybrid-Cloud” Architectures

The industry is embracing Heterogeneous Computing.

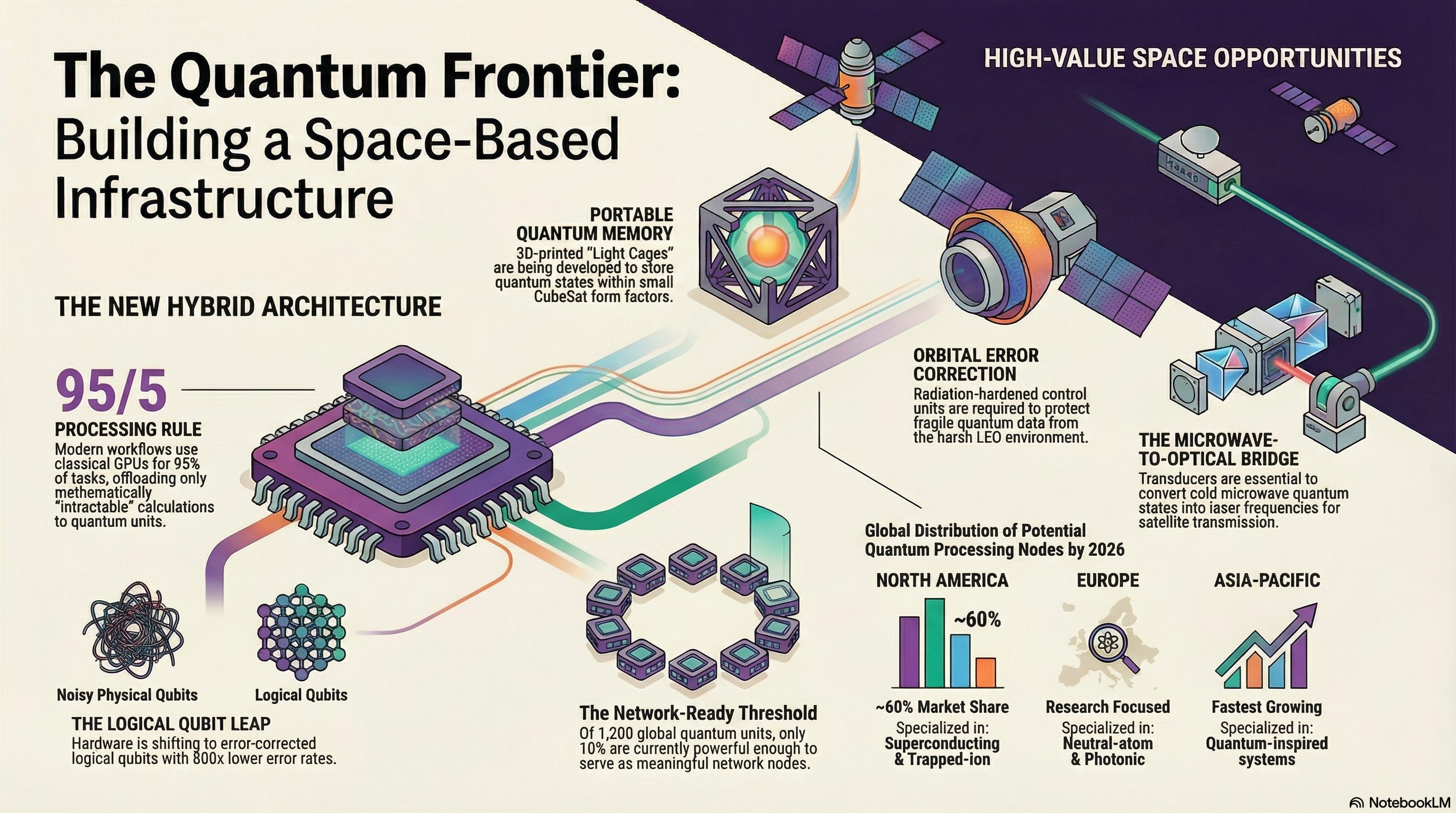

The 95/5 Rule:

In modern workflows, a standard GPU (like the NVIDIA Blackwell or Rubin architectures) handles 95% of the heavy lifting; data ingestion, classical pre-processing, and neural network training.

Only the most mathematically “intractable” 5% (such as calculating a specific molecular Hamiltonian or a high-dimensional optimization) is offloaded to a Quantum Processing Unit (QPU).

CUDA-Q and NVQLink:

NVIDIA’s CUDA-Q has become the industry standard for this orchestration.

By integrating with hardware-agnostic platforms like Classiq, developers can now synthesize quantum circuits that are automatically optimized for the specific backend they are using (superconducting, trapped ion, or neutral atom).

Orbital Integration:

This hybrid model could be the essential precursor to a space-linked network.

Satellites could act as the “Quantum Bus,” moving the 5% “quantum-only” data between global classical supercomputing hubs, creating a seamless, planet-scale hybrid computer.

B. Closing the “Quantum Talent” Gap

The scarcity of quantum physicists was once the primary bottleneck. The industry is bypassing this by abstracting the complexity through Low-Code/No-Code layers.

Algorithmic Synthesis:

Companies like Classiq and Zapata Quantum (which recently refocused on generative AI and industrial applications) provide functional modeling tools.

Instead of manually placing “Hadamard gates” or “CNOTs,” a software engineer can simply define a high-level intent (e.g., “Optimize this logistics route for 500 nodes”) and the software synthesizes the underlying quantum circuit.

From Physics to Engineering:

Organizations are no longer just looking for PhDs in Quantum Mechanics; they are hiring “Quantum Solutions Architects” and “Hybrid Workflow Engineers” who understand how to plug a QPU into a standard enterprise stack.

Democratic Access:

This abstraction allows traditional developers in the Pharmaceutical or Finance sectors to utilize quantum power without needing to understand the “Spooky Action” of entanglement, dramatically accelerating the time-to-market for quantum-enhanced products.

C. Industrialization over Physics

The industry is pivoting from a “brute force” race for high physical qubit counts to a sophisticated race for Fault Tolerance.

The Logical Leap:

A “Physical Qubit” is noisy and prone to decoherence. A “Logical Qubit” is an error-corrected unit composed of dozens or hundreds of physical qubits working together.

Google’s “Willow” Chip:

Recently demonstrated that increasing the number of physical qubits can exponentially reduce error rates, proving the feasibility of large-scale error correction.

Microsoft & Quantinuum:

Have successfully demonstrated logical qubits with error rates 800x lower than their physical counterparts.

The “Cargo” for Space:

This reliability is essential for space-based infrastructure. Attempting to send a “noisy” physical qubit through a satellite link is like trying to send a glass vase through the mail without a box.

Logical Qubits act as the “packaging”; they are stable enough to survive the transit through the atmosphere and the vacuum of space, ensuring the quantum state arrives intact at the destination node.

D. “Agentic AI” Synergy

A significant shift is the rise of Agentic AI; autonomous systems designed to reason, plan, and execute multi-step tasks within complex guardrails. Unlike traditional LLMs, these agents are “doers,” not just “talkers.”

The Computational Wall:

Agentic AI requires constant, real-time optimization. If a logistics agent is managing 5,000 autonomous drones, the “combinatorial explosion” of potential route changes, weather events, and battery constraints throttles even the most advanced classical GPUs.

Quantum-Enhanced Decisioning:

Quantum algorithms, particularly the Quantum Approximate Optimization Algorithm (QAOA), allow these agents to evaluate millions of potential pathways simultaneously.

“Quantum-Enhanced AI” (Q-EAI) is a fast-growing segment because it provides the “Brain Speed” necessary for true autonomy.

Agentic Self-Correction:

High-end adopters are using Agentic AI to manage the quantum hardware itself.

These AI agents monitor the QPU’s environment in real-time, performing Adaptive Error Mitigation; essentially “shielding” the fragile qubits by adjusting calibration parameters faster than a human operator ever could.

E. “Quantum-as-a-Service” (QaaS)

Quantum-as-a-Service (QaaS) is the primary entry point.

Lowering the CAPEX Barrier:

A standalone, error-corrected quantum computer still costs upwards of $50M–$100M to build and maintain.

QaaS allows firms to access this power for as little as $500 in “Trial Credits” (via Azure Quantum) or on a “Pay-per-Shot” basis ($0.01 to $1.00 per circuit execution).

The Hyperscaler Ecosystem:

AWS Braket:

Now provides a “Multi-Modality” menu, allowing users to switch between IonQ (Trapped Ion) and Rigetti (Superconducting) on the fly to see which hardware handles their specific AI agent better.

Azure Quantum:

Fully integrated with Copilot for Azure, allowing developers to write quantum code using natural language prompts. This is democratizing quantum access for standard enterprise developers.

IBM Quantum Network:

Focused on “Utility-Scale” computing, providing dedicated cloud access to their 1,121-qubit Condor and Osprey processors for Tier-1 industrial partners.

III. Global Quantum Hardware Estimates

For a space-based quantum infrastructure to be viable, there must be a sufficient density of high-performance “nodes” (quantum computers) to justify the investment. Currently, we are transitioning from a world of isolated experimental labs to a distributed network of commercial and sovereign systems.

1. Current Global Inventory

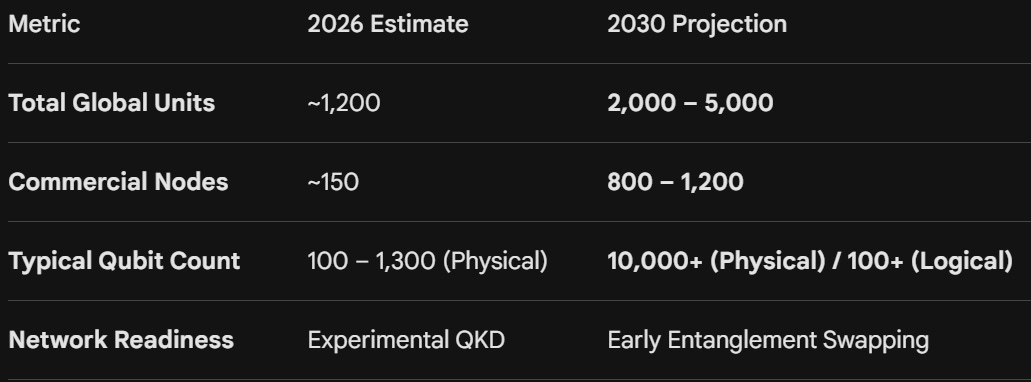

As of early 2026, the global census of quantum computers is around 1,000 to 1,200 functional units worldwide:

Cloud-Accessible Commercial Units (~100–200):

Systems from leaders like IBM, Google, Rigetti, and IonQ. These are the primary candidates for early integration into an orbital network.

On-Premise Enterprise & Research Units (~150+):

High-performance systems located within national labs, defense departments, and Tier-1 research universities (e.g., the UK’s National Quantum Computing Centre or RIKEN in Japan).

Specialized/Educational Units (~700+):

Smaller-scale systems, such as desktop NMR quantum computers (like those from SpinQ), which are used for algorithm development and training but lack the power for high-value applications like drug discovery.

2. The 2030 Horizon

By 2030, the density of the network is expected to increase as hardware moves from the “NISQ” (Noisy Intermediate-Scale Quantum) era to early fault tolerance.

3. Geographical Distribution of Potential Nodes

The quantum network will likely follow a “hub and spoke” model dictated by existing technological concentration.

North America (~60% market share): Dominated by the US, focusing on superconducting and trapped-ion modalities.

Asia-Pacific (Fastest Growing): Led by China’s massive state-funded initiatives and Japan’s industrial focus on quantum-inspired and superconducting systems.

Europe: Strong focus on neutral-atom systems (Pasqal) and photonic nodes (Oxford Quantum), which are inherently more “network-friendly” as they operate at room temperature or use light as the primary qubit carrier.

4. The “Network-Ready” Threshold

A catalyst for space-based quantum optics will be the arrival of Photonic Quantum Computers. Unlike superconducting systems that require massive dilution refrigerators, photonic systems (from companies like PsiQuantum or Xanadu) use light to process information. This makes them naturally compatible with the lasers used in Free Space Optics (FSO), allowing for a seamless transition from the processor to the satellite uplink.

While there are over 1,000 systems today, only about 10% are estimated to be currently powerful enough to serve as meaningful “processing nodes.”

The space-based strategy should therefore prioritize linking these high-value hubs first, creating a “Quantum Backbone” before expanding to smaller institutional nodes.

IV. Opportunities for Space Innovators

While the “Quantum Cloud” giants (IBM, Google, Microsoft) dominate the high-level compute, the enabling infrastructure (the hardware that makes the space-to-ground link possible) will be built by a new generation of agile startups and specialized engineering firms.

1. Quantum Memory & Synchronization (The “Buffer” Problem)

Photons are “transient”; they disappear the moment they hit a detector. To create a global internet, we need Quantum Buffers that can hold a qubit’s state in orbit while waiting for a ground station to come into view.

The Innovation:

3D-printed “Light Cages” (nanoprinted structures filled with atomic vapor) that can store quantum states at room temperature, fitting into a 3U CubeSat form factor.

The Opportunity:

Developing Portable Quantum Memories. Current systems use bulky “atomic vapors” or “cryogenic crystals.”

Innovation Gap:

We’re seeing the rise of 3D-printed “Light Cages” (nanoprinted structures filled with atomic vapor) that can store quantum states at room temperature.

Startups like SpeQtral and researchers at Humboldt University are leading this, but we lack high-volume, space-hardened manufacturing for these components.

Example Customers:

Sovereign Space Agencies:

ESA, NASA, and JAXA for long-range entanglement distribution.

Tier-1 SatOps:

SES and Intelsat looking to add “Quantum-Memory-as-a-Service” to their existing telecommunications constellations.

Potential Pricing:

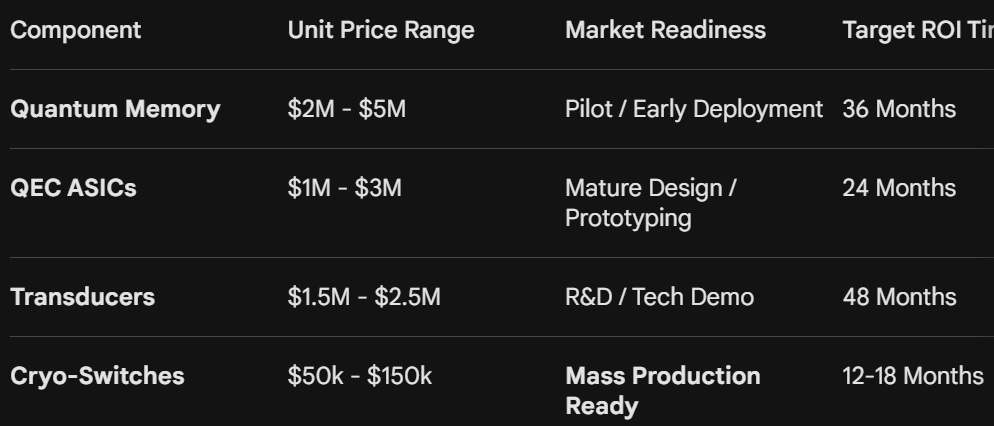

Hardware: $2M – $5M per unit for space-hardened, integrated memory modules.

Licensing: $500k/year for synchronization software and orbital calibration updates.

2. Orbital Error Correction (The “Logical Shield”)

In space, radiation and thermal fluctuations cause “decoherence” faster than on Earth. Raw physical qubits are too fragile for the journey; they must be wrapped in Error Correction codes to become “Logical Qubits.”

The Innovation:

Radiation-Hardened Quantum Control Units (QCUs).

These are ASICs (Application-Specific Integrated Circuits) that perform “Surface Code” decoding at the hardware level in real-time.

The Opportunity:

Hardware-Encoded Error Correction. Instead of using software-heavy classical overhead, innovators are building chips that perform “Surface Code” error correction directly at the hardware level.

Innovation Gap:

Companies like Riverlane and neQxt are pioneering the “QuOps” metric (error-free Quantum Operations).

The gap lies in Radiation-Hardened Quantum Control Units that can execute these correction cycles in the harsh LEO environment without the chip itself failing.

Example Customers:

Quantum Cloud Providers:

Microsoft and IBM for their orbital “Edge” processing nodes.

Defense Contractors:

Northrop Grumman or BAE Systems building “zero-trust” quantum communication satellites.

Potential Pricing:

Custom Chipsets:

$1M – $3M per flight-ready QEC module.

IP Licensing:

$10M+ for multi-year “Right-to-Use” agreements for proprietary decoding architectures (e.g., Riverlane’s Deltaflow stack).

3. Quantum Transduction (The “Frequency Bridge”)

Most quantum computers (like those from IBM or Google) operate at microwave frequencies (millikelvin temperatures), but space communication requires optical frequencies (lasers). We need a “bridge” to convert one to the other without losing the quantum state.

The Innovation:

High-efficiency Thin-Film Lithium Niobate (TFLN) or Rydberg Atom transducers integrated into a “plug-and-play” satellite bus interconnect.

The Opportunity:

Microwave-to-Optical Transducers. This is the “modem” of the quantum age.

Innovation Gap:

Currently, transduction efficiency is low and introduces noise. Innovators using Thin-Film Lithium Niobate (TFLN) or Rydberg Atoms are showing promise for high-efficiency conversion.

There is a emerging market for integrated “Quantum Interconnect” modules that could be bolted onto existing satellite buses.

Example Customers:

Commercial Quantum Hubs:

Amazon (AWS Braket) for linking their heterogeneous quantum hardware via satellite.

National Labs:

Oak Ridge (USA) or RIKEN (Japan) building intercontinental quantum testbeds.

Potential Pricing:

Transduction Modules: $1.5M – $2.5M per terminal.

Maintenance: $250k/year for cryo-optical alignment and calibration services.

4. Space-Hardened Cryogenic Switching (The “Cold Router”)

Even with passive cooling, high-performance quantum nodes require active thermal management and signal routing at near-absolute zero.

The Innovation:

MEMS-based Cryo-Switches (like those from the Menlo Micro & Rosenberger 2026 partnership) that operate at 10 millikelvin with near-zero thermal signatures.

The Opportunity:

Low-Power Cryogenic RF Switches. Traditional mechanical switches generate “Joule heating,” which destroys qubit coherence.

Innovation Gap:

The opportunity lies in Scalable Cryo-CMOS Controllers that bring the “brain” of the computer into the cold-box, eliminating the heavy wiring “heat-leaks” of traditional systems.

Example Customers:

Deep Space Mission Planners:

For quantum sensing on lunar or Mars-orbiting platforms.

Satellite Manufacturers:

Thales Alenia Space and Airbus for next-gen quantum relay satellites.

Potential Pricing:

Component Level: $50,000 – $150,000 per multi-channel switch.

Integrated Sub-systems: $2M+ for a fully redundant, space-qualified cryogenic routing assembly.