Space Forge: In-Space Manufacturing [Case Study]

By scaling ForgeStar iterations and proving reusability, the company aims to capture a share of the £10B+ advanced materials market

Space Forge’s journey from a Cardiff-based idea to a leader in Reusable Orbital Manufacturing (ROM) offers critical, actionable insights for founders seeking to industrialize microgravity production.

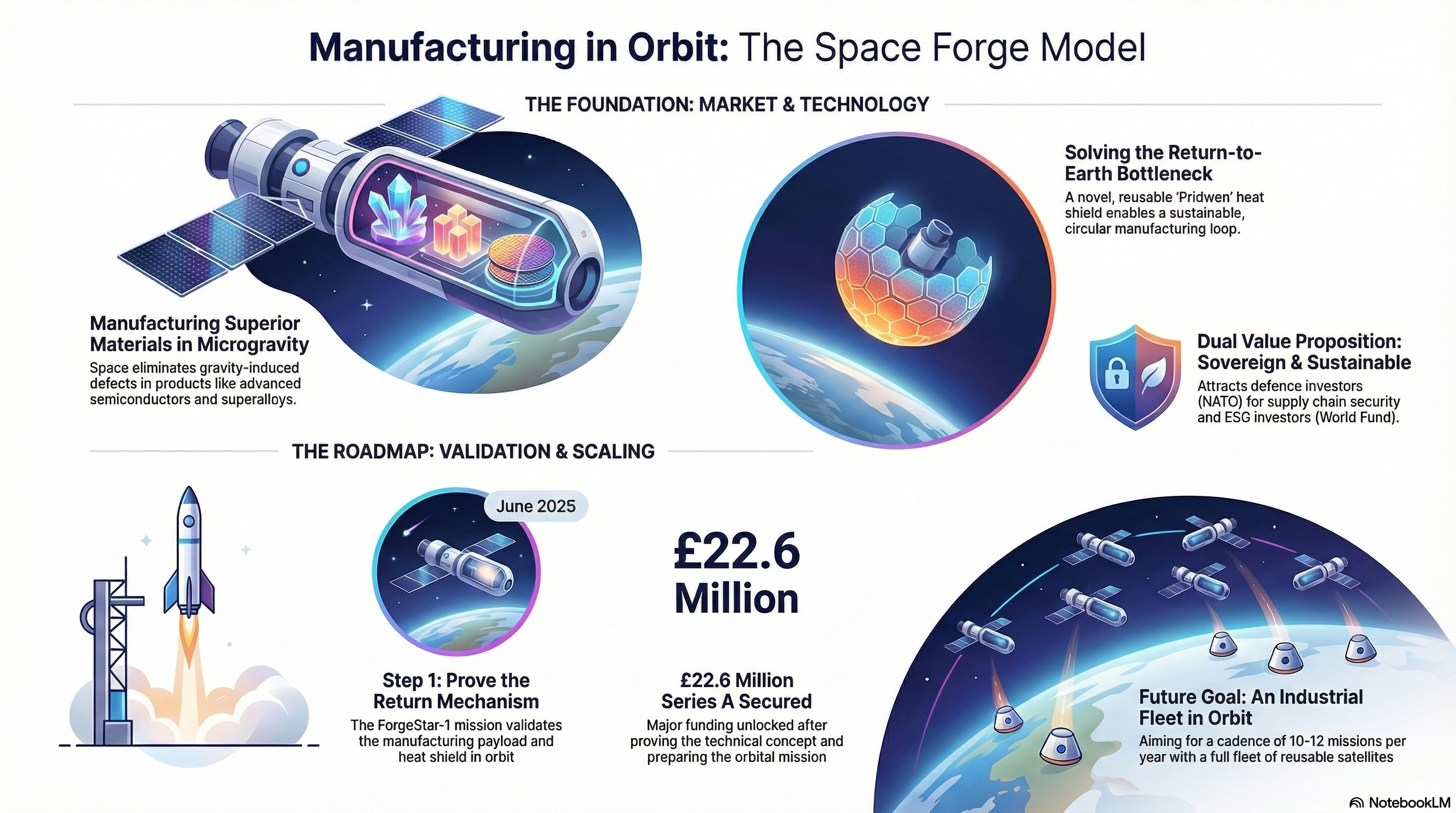

The model is built on solving the crucial Return-to-Earth bottleneck to create a circular space economy.

I. Market Research: Identifying the High-Value Non-Terrestrial Product

Founders must first validate that their product’s superior performance justifies the unique logistical cost of space.

1.1 Segmentation by Material Performance Advantage:

Initial Focus: Semiconductor Materials: The key target is compound semiconductors, where microgravity eliminates defects, enabling superior performance (e.g., up to 75% reduced energy usage in power electronics).

Actionable Insight: Focus on partnerships (e.g., United Semiconductors LLC) to establish clear routes to market and integrate space-grown materials into the existing terrestrial supply chain (e.g., for quantum computing, power electronics).

Future Focus: Expand into superalloys, advanced materials, and biotech products that require the vacuum and microgravity environment.

1.2 The Sovereign and ESG Value Proposition:

Sovereign Resilience: Strategic alignment and funding (led by NATO Innovation Fund, NSSIF) position the company to support national semiconductor strategies and secure resilient supply chains for defense and critical infrastructure.

Sustainability: The reusable, non-ablative heat shield technology is marketed as a method to reduce the environmental impact of space manufacturing, appealing to ESG-aligned investors (like World Fund).

II. Venture Design: De-Risking the Reusability Loop

Space Forge’s early milestones demonstrate a phased approach to de-risking the return mechanism—the most complex and valuable component of the business model.

2.1 The Technical De-risking Sequence (Return First):

Phase A: Ground and Sub-Orbital Validation: Used early grants (Innovate UK, UKSA) and private capital to test the core concept.

Milestone: Pridwen Heat Shield successfully trialed deployment on a zero-gravity flight (parabolic flight) to validate the novel origami-based design.

Phase B: First Orbital Validation (ForgeStar-1 Mission):

Goal: The ForgeStar-1 mission (“The Forge Awakens”, launched June 2025) was a one-way flight designed to: Activate the manufacturing payload and perform a full dress rehearsal for the Pridwen shield deployment in orbit (though the satellite itself was not designed to return).

2.2 Blended Funding Model for Scaling:

Record-Breaking Series A: The £22.6 million Series A (May 2025) was secured after the Pridwen concept was validated and the ForgeStar-1 mission was prepared.

Actionable Insight: Use non-dilutive funding (grants, UKSA) to prove technical feasibility, and leverage orbital demonstration (ForgeStar-1) and strategic defense backing (NATO NIF) to unlock the large private capital required for fleet scaling.

III. Execution Risk & Mitigation

The central risk is the reliability and cost of the re-entry and refurbishment cycle, which must be addressed to achieve a commercially viable operational cadence.

3.1 Technical Risk: Reusability and Refurbishment:

The Problem: The business model relies on a minimal refurbishment timeline to amortize high capital costs. Damage to the heat shield or structure during re-entry would destroy the financial model.

Mitigation: The Pridwen Heat Shield is explicitly non-ablative. This novel, origami-based design minimizes degradation, drastically reducing refurbishment time and cost compared to traditional, single-use ablative capsules.

3.2 Regulatory Risk: Re-entry Approval:

The Problem: Securing a regulatory license for routine, high-cadence re-entry and landing, particularly in the UK, is extremely complex and time-consuming.

Mitigation: The ForgeStar-1 mission focused on collecting safety data, including a monitored de-orbit using the Pridwen shield. This data is critical for proving aerodynamic control and orbital decay predictions needed for Part 450-style commercial re-entry licenses.

3.3 Competitive Risk: The U.S. Head Start:

The Problem: U.S. competitor Varda Space Industries has a significant lead, having successfully returned multiple capsules to Earth (under the FAA’s Part 450 license) and secured substantial funding ($329M total).

Mitigation: Space Forge focuses on semiconductors (a market Varda is only now pivoting to) and uses a novel, zero-emissions re-entry technology (Pridwen), while Varda relied on outsourced, legacy NASA-derived heat shield tech. Space Forge’s focus on sovereign resilience (UK/NATO) provides a strategic funding and customer base Varda does not directly address.

IV. Detailed Capabilities: The ForgeStar Platform & Operational Roadmap

The ForgeStar platform is a multi-generational system designed to achieve a high-cadence, circular manufacturing ecosystem.

4.1 Current Demonstrated & Operational Capabilities:

Manufacturing Payload Readiness: Confirmed successful activation of the payload designed to create the optimal environment for semiconductor crystal growth in microgravity (validated by ForgeStar-1 data).

Pridwen Heat Shield (Non-Ablative Re-entry):

Technology: Novel, origami-based, non-ablative reusable heat shield.

Advantage: Leads to zero emissions and lower refurbishment costs for reusability. Its deployed “shuttlecock” shape also aids passive stabilization.

4.2 Projected Future Capabilities & Industrial Fleet Cadence:

ForgeStar-2 Development: Next-generation platform with larger payload capacity and improved reusability designed to produce materials with a value exceeding the cost of the launch.

Cadence Target: The long-term plan is to establish a flight cadence of 10-12 missions a year (requiring a full ForgeStar fleet).

V. Commercial Partnerships Potential

Space Forge’s commercial success hinges on integrating the new space supply chain into the highly structured, multi-trillion-dollar terrestrial semiconductor and defense industries.

5.1 Semiconductor Supply Chain Integration:

United Semiconductors LLC: This partnership is crucial for establishing clear routes to market and integrating space-grown materials (crystal seeds) into the terrestrial wafer processing and manufacturing pipeline.

CISM (Swansea University): Partnership with the Centre for Integrated Semiconductor Materials provides access to critical terrestrial infrastructure for testing and scaling up the space-grown materials.

5.2 Strategic Aerospace and Defense Backing:

Northrop Grumman UK & Sierra Space: Agreements with these major aerospace and defense primes are designed to explore:

Integrating Space Forge’s advanced semiconductor materials into their aerospace and defense systems.

Collaboration on the Dream Chaser® Spaceplane and other space station technology, providing potential high-volume transport and testing opportunities.

5.3 Investor-as-Customer Validation:

The NATO Innovation Fund (NIF) and other defense-aligned investors serve as a strategic customer base, ensuring that the development roadmap aligns with resilient and advanced military technology needs.

VI. Strategic Outlook: Scaling to a Circular Ecosystem

Scaling Challenge: The key business risk remains proving large-scale reliability of the re-entry and refurbishment cycles at fleet scale. Minimal refurbishment time is essential to amortize the high initial capital costs.

Commercial Goal: Circular Manufacturing: The long-term vision is a Circular Manufacturing Ecosystem where satellites are rapidly recovered, refurbished, and relaunched, positioning the company as the world’s first returnable and reusable satellite platform provider.